Mr. Vinay Paharia

Chief Investment Officer - Equity, PGIM Mutual Fund.

Vinay Paharia joined PGIM India AMC in January 2023 and is currently the Chief Investment Officer at PGIM India Mutual Fund. He has over 22 years of experience in equity market and fund management. He holds M.M.S, BCom and CFA (ICFAI) degrees. Vinay has been a growth investor and has followed a consistent investment philosophy of buying good quality and high growth companies at a reasonable price. This strategy has been an evergreen framework and has outperformed markets most of the times (but not all the time). His objective is to buy companies that are available at a price that may be slightly lower than the underlying fair value, which presents a greater potential upside over a five-year period. Vinay vouches for a disciplined, evidence-based investment approach over chasing short-term returns.

Please note we have published the answers as it is received from the Fund Manager of PGIM Mutual Fund.

Q1. With India’s valuation premium over other emerging markets moderating and GDP growth expected to remain strong (~6.8% in FY27), how do you assess the current risk-reward for long-term equity investors? Within this backdrop, which segments-large caps, mid caps, or small caps-appear relatively better positioned today from a valuation and earnings growth perspective?

Ans: Last few months have been a macro stress test - combining oil shock, capital outflows, currency pressures, AI related growth pangs and growth downgrades in a short span. However, we believe, many of these being transitory and would resolve itself with passage of time, timelines however are uncertain. More importantly, the above has resulted in a meaningful correction in the markets and much of the froth in valuations which was built has been taken away which is being reflected in the price. Largecaps and Smallcaps are now trading very close to their longer term averages in terms of valuation and risk-reward is much more balanced than before. However, Midcaps are still trading at moderately rich valuations and are hence less preferred compared to large caps and small caps. We believe, it is a good time to increase allocation to Indian equities. It is important to remember that timing is very difficult and investing when risk-reward is favorable is likely to be more fruitful. More importantly, the risk-reward is highly favorable for high growth and good quality business, wherein valuation as well as earnings growth both are in favor for long term investing.

Q2. With passive AUM continuing to rise in India, where do you believe active management can still consistently generate alpha? Are there specific market segments or conditions-such as higher dispersion or volatility-where active strategies have a clear edge over passive?

Ans: Active management's fundamental premise remains robust: markets are not completely efficient, and skilled managers can exploit these inefficiencies to generate risk-adjusted returns above benchmark indices. The strengths of active investing include:

1. Alpha Generation Potential: Skilled active managers can capitalize on market inefficiencies, behavioural biases, and information asymmetries that passive strategies cannot exploit. During periods of significant market stress or structural changes, active managers can potentially protect capital and identify opportunities thereby generating alpha.

2. Risk Management Flexibility: Active managers possess the ability to adjust portfolio risk dynamically, reducing exposure during periods of heightened volatility or when valuations appear stretched. This tactical flexibility can be particularly valuable during market transitions that indices cannot anticipate.

3. Access to Unique Opportunities: Active strategies can invest in securities or sectors before they enter major indices, potentially capturing returns during the inclusion process. They can also avoid or underweight deteriorating companies that indices must hold until they are removed.

We expect polarized performance from the markets. We expect high growth and high quality buckets to outperform while the low growth/quality bucket to underperform and give away the excesses which were built in FY24. Passive investing means there is some degree of exposure to low growth and low quality stocks as they make up a significant portion of Indexes. Active investing ensures conviction and exposure largely to high growth and high quality stocks.

Q3. As we approach the upcoming earnings season, what is your outlook on corporate earnings growth? Which sectors or themes are likely to drive the next phase of market performance, and where do you see the key downside risks?

Ans: We think we are once again likely to witness an earnings impact like that in the pandemic period. In March 2020 to June 2020 quarter (the first quarter of pandemic), we witnessed massive cuts in Nifty 50 Index 1-year forward earnings expectation, from a growth in double digits (in line with historical performance) to an almost 15% decline. However, once again, this is only likely to be transient (like the pandemic) and not structural. Hence we do not expect a material long term structural impact on the macroeconomic environment. The actual earnings compounded at 15% per annum from March 2020 to March 2026, highlighting the transient impact of the pandemic. We feel the longer term earnings trajectory is unlikely to be impacted even this time, with only a short term transient impact likely due to the current geo political environment. Even a massive cut in short-term earnings can only have a small impact on overall Fair Values of companies. This is because equities are growing annuities valued till perpetuity.

Overall fabric of the market constructive for growth + quality investing for the long term. Preferred sector plays are more domestic oriented – Consumption, Domestic financials, India Healthcare, Telecom. Cautious/Negative on I.T, deep cyclicals, Energy and Utilities

Q4. SIP inflows have remained resilient, touching record highs even during volatile phases. Do you see this as a structural shift in investor behaviour? During market corrections, would you advise investors to maintain, increase, or rebalance SIP allocations-and what factors should guide that decision?

Ans: Investment decisions are shaped not only by returns or market data, but also by individual behaviour. Risk tolerance, time horizon, and emotional responses play a significant role in how investors act, especially during volatile markets. We advise investors to maintain staggered investments for all segments of the market.

Periods of geopolitical uncertainty, such as the conflict unfolding today, often lead to higher market volatility and heightened investor reactions. It is common for investors to consider redeeming investments prematurely, trying to time the market, or pausing allocation decisions altogether. While these responses are natural, history shows that emotionally driven decisions

often work against long-term financial goals. Our internal study of Nifty 500 TRI shows that investors who stayed invested 04-Sep-2001 to 31-Dec-2025) during this period, earned 17.33% return while investors who missed the best 20 days ended up earning just 11.06%. This means that investor who stayed invested, (assuming a lumpsum investment of 1 lakh), made Rs 48.77 lakh at the end of 24.32 years. The investor who missed 20 days accumulated Rs 12.82 lakh, a difference of (Rs-35.95 lakh).

Q5. Many investors chase recent outperformers, especially in mid- and small-cap funds, often misaligning with their true risk appetite. What framework would you recommend for selecting equity funds and ensuring portfolios remain aligned with risk tolerance? How can investors stay disciplined through market cycles?

Ans: We have been strong proponents of Growth Investing in India. Our definition of Growth Investing is as follows:

"Investing in a well-diversified portfolio of companies that demonstrate above average growth in business, while generating above average return on equity, purchased at a reasonable price"

Growth investing is all about buying good businesses at fair price. Returns for growth investors are largely driven by earnings growth. Growth investors do not bet on valuation re-rating, but on fair value growth. India is one of the fastest growing large economies in the world. Thus, we have a higher probability of finding superior growth companies in India. We have a large number of companies generating higher than their cost of equity, thereby creating superior shareholder value. We have also witnessed IPOs of a large number of good quality and high growth new age businesses in Indian bourses. Indian companies on average have generated a healthy return on equity (RoE) while growing at a reasonable pace. Over the Long term (two decade) average RoE generated by Top 500 companies in India is 15%. Similarly, long term average sales growth has been 12% for the same set.

We tend to be overweight on the Consumer Discretionary and Healthcare Sectors, as the stocks within these sectors align with our investment philosophy.

Q6. What are the non-negotiable factors your team looks for when selecting stocks? Specifically, how do you evaluate management quality and governance to ensure businesses can sustain performance across cycles?

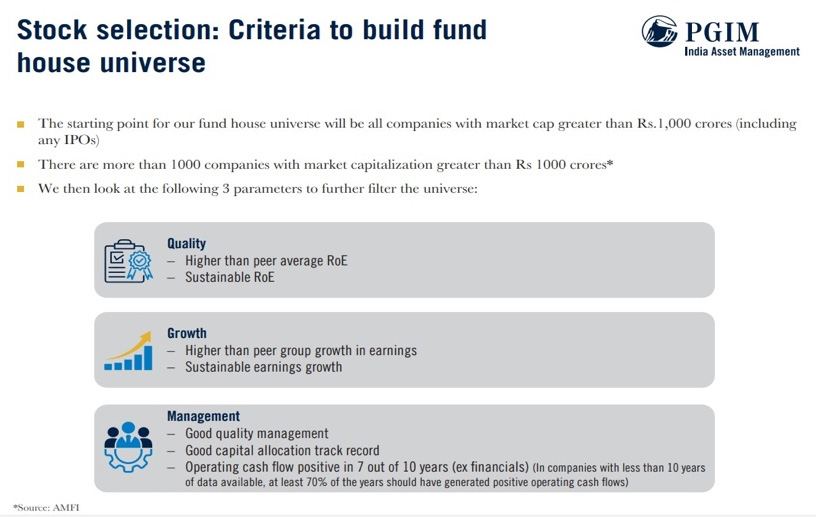

Ans: Our framework excludes low-growth and low-quality stocks, and it is applicable on all sectors.

Our evaluation of management quality is in conjunction with the quantitative measures stated above and promoter background checks, as well as internal risk triggers. We also take a holistic view from the Fixed Income Team on rating wherever applicable and relevant

Source: Internal Research

Mutual fund investments are subject to market risks, read all scheme-related documents carefully.

Mr. Venugopal Manghat

Chief Investment Officer - Equity, HSBC Mutual Fund.

Venugopal Manghat is the Chief Investment Officer (CIO) - Equity of HSBC Mutual Fund. Venugopal was previously Head - Equity Investments, L&T Investment Management Limited from May 2016 to Nov 2022 and was Co-Head - Equity Investments, L&T Investment Management Limited from Apr 2012 - Apr 2016. Prior to 2012, he was Co-Head - Equities, Tata Asset Management Limited, India from 1995 - 2012. His educational qualification is MBA Finance, B.SC.

Please note we have published the answers as it is received from the Fund Manager of HSBC Mutual Fund.

Q1. Recent geopolitical tensions in the Middle East have once again raised concerns around global market volatility. From the perspective of Indian equities, do such events generally result in only short-term market disruptions, or can they have any lasting implications for the long-term outlook of the Indian economy and markets?

Ans:1 Indian markets have historically "climbed the wall of worry" through a wide range of internal and external concerns such as wars, commodity spikes, tech bubble, Global Financial Crisis, and Covid. Such events often result in market corrections in the near term, but markets recover as fundamentals reassert themselves.

Importantly, periods like these tend to separate the 'wheat from the chaff'. High-quality companies, i.e., those with strong balance sheets, disciplined capital allocation, resilient business models, and credible management teams, often use volatility to consolidate market share, strengthen stakeholder relationships, and emerge in a better competitive position once conditions normalise.

From a longer-term perspective, we believe India is better placed today to absorb external shocks than it was in prior cycles. Over the past decade-plus, a series of reforms and institutional strengthening across sectors has helped build a more durable foundation.

So, while near-term market moves can be sharp and sentiment-driven, we don't see such episodes, by themselves, changing the long-term trajectory of the Indian economy or the structural trend in equities.

Q2. After a prolonged phase of FII outflows, February witnessed the highest foreign inflows into Indian equities in nearly 17 months. Do you believe this signals a more sustained improvement in global investor sentiment toward India, or could such inflows remain intermittent in the near term?

Ans:2 Foreign investor positioning in India is typically driven by a combination of India-specific fundamentals and the broader global/emerging market opportunity set.

A key reason India saw meaningful outflows over the past year was the global concentration of returns in the AI theme. Markets such as US, Taiwan, Korea and parts of China have a larger share of direct AI beneficiaries, whereas India has fewer "pure-play" AI winners in the listed space. Currency dynamics also mattered. At the same time, India's earnings growth expectations softened versus its long-term trend.

Looking ahead, consensus expects earnings to re-accelerate to mid-teens growth in FY27E from single-digit growth over past two years. Valuations have also become more reasonable with India's valuation premium to MSCI EM moderating closer to long-term averages. Finally, FII positioning is light with India's active weight relative to the EM index near multi-decade lows. All these can create durable improvement in positioning with strong incremental inflows.

Net-net, while February's strong inflows are encouraging, we'd expect the near-term pattern to remain somewhat stop-start, with flows reacting to global risk appetite, geopolitics, US dollar, and relative performance across markets. We expect FII positioning to improve over the medium term.

Q3. The IT sector has witnessed a sharp correction recently, with the index declining by nearly 20%, partly driven by concerns around evolving technologies such as artificial intelligence and their potential impact on traditional IT services. From a long-term perspective, how do you evaluate these developments and the future growth prospects of the Indian IT sector?

Ans:3 The recent correction in Indian IT has been sharp with >20% drawdown during YTD2026.

From a top-down lens, the sector is facing genuine headwinds as AI systems become more capable moving from "assistive" tools to autonomous agents. This uncertainty is likely to stay elevated over the next few quarters as technology and adoption curve evolves quickly. However, the bottom-up picture is more balanced. Many IT companies delivered in-line to better-than-expected 3QFY26 results, with healthy deal wins and management commentary that remains broadly constructive.

Over the medium term, we see AI as both a disruptor and a growth driver. On one hand, it can compress some legacy work through automation and productivity gains. On the other, it can expand the addressable market as enterprises push into "agentification" (embedding AI agents across workflows). Though valuations have reset closer to long-term multiples, in the near term, continued developments in Agentic AI could keep sentiment and valuations subdued.

Ultimately, the key long-term question is whether AI meaningfully lowers the sector's terminal growth rate and if so, by how much. The answer to that, relative to the valuation investors are paying today, will determine whether this correction proves to be a temporary derating or a more lasting reset.

Q4. The recent regulatory changes introduced by SEBI allow equity schemes to allocate a limited portion of assets to commodities such as gold and silver through ETFs. How do you view this flexibility from a portfolio construction perspective, and do you see it meaningfully influencing diversification within equity-oriented funds?

Ans:4 SEBI's recent move to allow equity mutual funds greater flexibility permitting allocation of up to 35% to instruments such as gold and silver (via ETFs), as well as InvITs and debt broadly expands the options available to fund managers. This gives managers additional levers to manage liquidity, drawdowns and diversification, particularly during periods when equity risk premium increases.

That said, in our view, the most important principle is that an equity scheme should remain true to its stated mandate and investor expectations. For example, a small-cap fund is typically chosen to participate in India's growth story through smaller companies that can scale over time. If such a fund were to meaningfully increase exposure to gold or debt, it could dilute the very equity participation investors signed up for.

As a fund house, we maintain cash primarily to meet redemption needs and don't take large active cash calls. Similarly, while a small allocation to gold/silver ETFs or other permitted instruments can provide incremental diversification, it's unlikely in our funds to become a meaningful portion of equity portfolios.

Overall, the change is a positive, but whether it materially changes diversification within equity schemes will depend on each fund's philosophy.

Q5. Markets periodically witness events that can trigger short-term volatility. Given that such events are a recurring feature of markets, how should investors approach these phases so that they view them as opportunities rather than panic and remain focused on long-term wealth building?

Ans:5 Over the past four decades, two things have remained remarkably constant - Equities have been volatile in the short term, and they've tended to outperform most other asset classes over the long term. In the short run, every volatile event feels different and permanent, however, most have been temporary within a longer compounding journey.

The most practical way for investors to turn volatility into opportunity is to shift towards a process-oriented approach to equity investing rather than reacting to daily news flow. Use systematic investing through SIPs/ STPs and staggered deployment to help manage volatility. During such volatile periods, strong businesses with resilient balance sheets and cash flows tend to recover faster and compound better. Investors should maintain adequate liquidity so that short-term market moves don't result in forced selling and become permanent losses.

Empirical evidence suggests that some of the best long-term returns are earned by investing when sentiment is weakest. To conclude, volatility creates uncomfortable moments, but it also creates better entry points for long-term wealth building.

Q6. It is often observed that investors gravitate toward schemes that have delivered strong recent performance and may even switch funds based on short-term rankings. In your view, how should investors approach fund selection and avoid the common behavioural trap of chasing past performance?

Ans:6 Styles, sectors and market caps rotate as macro conditions change. So what worked for a fund in one phase may not work in the next. A fund that tops the charts in a momentum-led rally may lag when leadership shifts to value, quality, or defensives. If investors focus on only one element (typically recent returns) and switch schemes based on short-term rankings, the outcome is often sub-optimal.

A better approach is to evaluate whether a fund's investment philosophy and process fits the investor's needs. Practically, investors should look at:

Consistency across market cycles, rather than just short-term returns

Risk-adjusted performance and not only absolute performance

Portfolio construction discipline (diversification, concentration, turnover)

Fund house and portfolio manager process (stability in investment approach)

Costs and tax efficiency

In short, investors are better served by choosing funds with a clear, well-executed process aligned to their needs and then giving that process time to work rather than switching based on recent rankings.

Source: Internal Research

Mutual fund investments are subject to market risks, read all scheme-related documents carefully.

Mr. Shriram R.

Chief Investment Officer - Fixed Income, HSBC Mutual Fund.

Mr. Shriram R.,CIO - Fixed Income, overseeing the management of about INR40,000cr (~USD 8bn), in assets across various Fixed income and Hybrid funds (INR only). He has been in the Asset Management business since 2001 and has over 22 years of experience in fixed income markets. Prior to joining HSBC Asset Management, he was Head of Fixed Income at L&T Investment Management Limited (2012-2022). From 2010-2012, he was Portfolio Manager at Fidelity (FIL) Fund Management managing their India domiciled INR FI funds. From 2005-2009, Shriram was based in Hong Kong at ING Investment Management Asia Pacific, where he managed multi currency portfolios as Senior portfolio Manager, Global EMD (Asia) - co-managing the Asian portion of Emerging Market Debt funds, with focus on sovereign HC and LC rates/ FX, as well as pure Asia local currency funds / mandates. His earlier assignments were with ING Investment Management India as Fixed Income Fund Manager, Zurich Asset Management Company in fixed income research and with the Treasury department of ICICI Ltd, where he started his career in investments in 2000. Shriram is a Chartered Financial Analyst and holds a Post Graduate Diploma in Business Management from XLRI Jamshedpur and an Engineering degree from the University of Mumbai.

Please note we have published the answers as it is received from the Fund Manager of HSBC Mutual Fund.

Q1. Debt is considered an important component of asset allocation. From a long-term portfolio perspective, how should investors think about the role of debt funds in balancing risk and stability within their overall investment strategy?

Ans:1 Debt funds play an important role in any investor's portfolio asset allocation. They tend to be relatively less volatile and may have the ability to generate potential returns depending on debt funds have acted as an alternate for the traditional FDs. volatility. Depending on the investor's risk taking ability, need for liquidity and investment time horizon, volatility range of debt funds of

varying risk - return profile from which to choose from.

Q2. Global interest-rate movements, particularly those of the US Federal Reserve, often influence capital flows and bond yields across emerging markets. How do you assess the potential impact of global monetary policy developments on the Indian fixed-income market?

Ans:2 Global monetary policy-especially the Fed-affects Indian fixed income mainly through US Treasury yields and global risk premia, which influence the level and shape of the G-sec and swap curves, and through capital flows into EM debt. Hence, a more hawkish global backdrop tends to tighten financial conditions via higher term premia, weaker risk appetite and a firmer USD. This eventually can increase INR hedging costs and also add to FX volatility. For rates market, it can push yields higher. The recent geopolitical developments have trickled down to rates - FX and interest rate channels - as the concerns around energy-led inflation pressures could imply delayed or no rate cuts by the US Fed, which was not the case until before the West Asia war.

Having said that, the surge in yields in EM's incl. India has been far lower than that observed in the AE's - as EM's fiscal, debt and inflation indicators are better placed than many AE's. Hence, even as the nominal interest rate differentials are lower, narrower than the past, the real differentials are still better. Therefore, even as the global policy tightens, esp. of the US Fed, the implications on Indian debt markets is likely to be contained; benefiting from strong macro fundamentals such as that of near-target inflation, continued fiscal consolidation and decent growth momentum. The duration of the Middle East crisis could turn out to be a spanner in the wheel as uncertainty leads to higher risk premia, globally. As a net energy importer, we could see spillover effects through the FX channel which could then permeate into external, inflation and fiscal risks. At this juncture, inflation and fiscal risks are still contained with external sector far more exposed.

Q3. India's corporate bond market has been gradually evolving, with increasing participation from institutional investors and improving regulatory frameworks. How do you see the development of the corporate bond market shaping opportunities for debt mutual funds over the long term?

Ans:3 Corporate Bond market has been gradually evolving over the years. Various reforms by SEBI, CCIL and RBI which include online Government securities and bond platforms, RFQ trading, and tri-party repos, have boosted liquidity. Corporate issuances hit record highs in FY25, fueled by RBI rate cuts and infrastructure needs, with projections to exceed ₹100-120 trillion by 2030. Outstanding bonds grew at a 12% CAGR over the past decade, rivaling bank credit mobilization. With the continued awareness of the bond market and proper categorization of the debt funds (as per the investment horizon of an investor), debt funds have acted as an alternate for the traditional products. With more participation from the institutional and retail investor, bond market has become more liquid thus reducing the liquidity risk.

Q4. In a credit market where external ratings may lag real developments, what does your in-house credit evaluation framework look like - and how do you assess a company's true debt-servicing ability?

Ans:4 We have our own internal rating framework/scale and limits for long- term (AAA to BBB) and short-term instruments (ST1 highest to ST5 lowest), driven primarily by standalone credit strength. The assessment centers on long-term debt-servicing capacity, factoring in business cyclicality (where relevant) and foreseeable events that may drive material cash outflows/inflows (e.g., M&A, capex). Our structured rating review covers business and financial fundamentals, forecasts and stress tests, promoter track record, mutual fund exposure, rating sensitivities, rating history, and discussions with management and rating agencies-supported by internal governance and sanctions screening.

Following unexpected negative events, the first priority is to evaluate liquidity, funding buffers, and financial flexibility available with the issuer to absorb short-term stress before making internal rating changes. Where risks are severe and persistent, the rating is immediately moved to sell or are placed on hold and incremental investments are paused until the hold is lifted. When warranted, internal ratings are upgraded or downgraded promptly, without waiting for external rating actions, to provide timely investment guidance to the trading desk. Ongoing monitoring is maintained through quarterly results, early warning indicators, external rating updates, and other material developments.

Q5. Given the wide range of debt fund categories available today, how should investors align their investment horizon and risk tolerance with the appropriate type of debt fund?

Ans:5 Investors should align their investment horizon according to their risk-taking ability and also the duration of the investment. For all the debt funds, risk matrix has been defined by SEBI which considers credit risk and interest rate risk. Risk averse investors should look for debt funds which invest in high rated securities and also lower maturity thus less sensitivity for interest rate risk. Given that we are close to the bottom of interest rate cycle, we believe it would be better for investors to keep duration risks low for the next 6-12 months.

Q6. SEBI has recently introduced sectoral debt funds. How do you interpret the role of this category within a fixed income portfolio, and what type of investors should ideally consider such strategies?

Ans:6 Sectoral debt funds (as a SEBI category) are best seen as a 'satellite' allocation within fixed income-not a core holding. They concentrate credit exposure in sector 1-2 (e.g., Financial Services, Energy, Infrastructure, Housing, Real Estate), so the portfolio's outcome is driven less by broad rate moves and more by sector-specific credit cycles, regulation, liquidity, and refinancing conditions. Investors who are having a basic understanding of the sector's business model, can tolerate sector concentration risk, and are using it as a satellite allocation through such concentrated products.

Source: Bloomberg, HSBC Mutual Fund, Latest available data as on 18 March 2026 unless otherwise mentioned

Past performance may or may not be sustained in future and is not a guarantee of any future returns.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Mr. Dhawal Dalal

President & Chief Investment Officer - Fixed Income, Edelweiss Mutual Fund.

Mr. Dhawal Dalal has 20 years of experience and an MBA from University of Dallas (USA). Mr. Dhawal has joined Edelweiss Asset Management Limited in the year 2016. He is responsible for the overall growth of fixed income assets through a healthy mix of retail and institutional clients. Before joining Edelweiss Asset Management Limited, he was the head of Fixed Income at DSP Black Rock Investment Managers Private Limited and led a team of Fund Managers managing fixed income assets. His role there was to expedite overall growth of fixed income assets, performance and client interactions.

When not occupied with work, he loves reading on emerging trends in the global markets, geo-political developments and books on behavioral trends. He’s also a movie buff and never misses a chance to watch a blockbuster with his near and dear ones. A humble and learned person, he strongly believes that every individual should have a sense of purpose in life!

Please note we have published the answers as it is received from the Fund Manager of Edelweiss Mutual Fund.

Q1. With a change in leadership at the US Federal Reserve expected around, how should global and Indian debt market investors think about continuity versus change in policy approach and market expectations?

Ans: Global financial markets are keenly awaiting the potential change in the thought process from the new Fed chair on their stance on inflation and the trade-off between AI-led productivity gains (which can lower inflation) and recent tariffs-led price gains (which may not have been fully passed through). The current Fed is perceived to be extra cautious on tariff-led uncertainties. If the new Fed chair can drive consensus on inflation trajectory to be lower, then Fed will be able to cut rates more aggressively. This will be bullish for global financial markets including Indian bond markets, in our view.

Q2. With the rupee experiencing phases of depreciation, how should debt mutual fund investors understand its impact on interest rates, inflation expectations, and fixed-income portfolio positioning?

Ans: INR’s recent depreciation is mainly due to FPI outflows and not due to any macroeconomic event. That said, the INR’s depreciation will have mild effect on our import basket amid the recent fall in crude oil while it will have a positive impact on our exports. As a result, the FY26 CAD is expected to be ~1% of the GDP, which will be within the tolerance zone even as the BoP will be in slight deficit for the second consecutive year. Overall, the recent move in the INR appears to be growth-supportive in our view and will not have any material negative impact on India’s growth-inflation dynamic, in our view.

Bond investors should, therefore, take advantage of the recent increase in bond yields in 2- to 3-year segment and lock in attractive rates with the investment horizon of at least one year as we expect the RBI to keep policy rates at current levels in CY2026.

Q3. With India’s inflation remaining well below the RBI’s medium-term target for an extended period, how should investors interpret this phase?

Ans: The recent decline in headline inflation in India has two main drivers – cyclical and structural. Cyclical drivers include above average monsoon for three years, lower crude oil prices and benign weather conditions. Together, they have contributed to lower food and energy prices which form the bulk of our inflation basket. Structural drivers include declining trend in nominal GDP growth, improvement in logistics, storage & transportation and maturing consumption patterns.

Taking all these together, we believe that India’s headline inflation is likely to experience lesser volatility as compared to the past and will likely remain in a range of 2% to 5% going forward.

Lower average inflation is relatively good for the investor in general as aggregate savings rate may improve.

Q4. Given that the FY27 fiscal deficit target is marginally lower, but gross market borrowings remain high, how do you see the net impact on long-term bond yields?

Ans: While FY27 gross borrowing is higher, the net borrowing is comparable to FY26 net borrowing. We believe that the bond market will have to reconcile this difference going forward as IGB maturities will rise every year going forward.

That said, we expect GOI’s debt to GDP ratio to gradually trend lower towards 50% by FY31 as highlighted in the new framework in the Union Budget. A lower government borrowing is always good news for the bond market. A declining trend in the government borrowing, overall improvement in fiscal health and strong & sustained economic growth in the next five years should lead to a gradual decline in bond yields barring any unexpected event risk, in our view.

Q5. Following the recent Union Budget’s increase in STT on F&O transactions, there has been discussion around its potential impact on arbitrage fund strategies. How do you assess this change, and what should investors understand about its implications for arbitrage funds?

Ans: Assuming there is no revision in the Budget proposal of revision in STT on F&O transactions, we expect a mild impact of ~30 bp on the annualized returns of arbitrage funds.

We believe that risk-reward ratio is still in favor of the investors of arbitrage funds on tax-adjusted basis as compared to other investment opportunities in the current market conditions.

Q6. What is your in-house credit research process? How do you assess a company's ability to pay, beyond just relying on external credit ratings?

Ans: Our credit assessment framework is based on multiple drivers such as analysis of key macro-economic factors, analysis of the sector followed by the analysis of the borrower.

Analysis of the macro-economic factors include analysis of the current fiscal landscape, monetary policy landscape, overall credit environment, current regulatory landscape, analysis of the banking system and overall term structure of rates

Our sector analysis includes the fiscal health of the sector, recent profitability trends, analysis of the dominant player & his pricing power, regulatory landscape pertaining to the sector, capacity utilization etc.

Analysis of the borrower includes deep dive into financial health, profitability trends, free cash flow, borrowing trends, quality of the leadership, their reputation and their business acumen, shareholding structure, trend in the market cap etc.

A thorough analysis of these factors provides us with a good understanding of the credit and the drivers of their underlying credit rating. We also continuously monitor the diversification of bond holders, recent trends in credit spreads, secondary market liquidity in bonds of the underlying credit and any material development either at the sector level or at the borrower level.

Source: Internal Research

Mutual fund investments are subject to market risks, read all scheme-related documents carefully.

Mr. Trideep Bhattacharya

CFA, President & Chief Investment Officer - Equity, Edelweiss Mutual Fund

Mr. Trideep Bhattacharya has a PGDBM in Finance from SP Jain Institute of Management & Research, Mumbai, a CFA charter holder and a B.Tech degree in Electrical Engineering from IIT Kharagpur. Mr. Trideep brings with him over two decades of experience in equity investing across Indian and global markets. Prior to joining Edelweiss AMC, he played a key role in building a market-leading PMS business at Axis Asset Management Company, where he served as Senior Portfolio Manager – Alternate Equities. He has also worked with reputed global institutions like State Street Global Advisors and UBS Global Asset Management in London, UK. Mr. Trideep is also a member of the Capital Markets Policy Council, a distinguished body instituted by the CFA Institute to guide its advocacy team on current and emerging policy issues impacting global capital markets. When not immersed in market trends and investment strategies, Mr. Trideep enjoys playing tennis, bridge, and experimenting with musical instruments.

Please note we have published the answers as it is received from the Fund Manager of Edelweiss Mutual Fund.

Q1. With India strengthening its global trade position through deeper engagement with the EU and a potentially more favourable tariff environment with the US, how do you assess the long-term impact of these developments on Indian equities and corporate competitiveness?

Ans: The recently concluded FTAs, along with the lowering of tariffs on exports to the US, augur well for Indian corporate earnings, as sectors such as textiles, pharmaceuticals, chemicals, aviation, and auto components stand to benefit from improved export opportunities. As India becomes more competitive relative to its peers, we expect a compression of the external risk premium, which in turn is likely to enhance foreign investor appetite and further improve the equity outlook.

Q2. There have been discussions around intermittent FII outflows from India, often attributed to factors such as currency movements, relative growth triggers, and tax considerations. How do you assess these concerns, and what could emerge as the next key triggers for renewed FII interest in Indian equities?

Ans: The recent FII outflows reflect a slowdown in India’s corporate earnings, driven by elections, higher interest rates, fiscal prudence, and prolonged monsoons. This coincided with near-term investment opportunities in the US (higher interest rates), Brazil (higher commodity prices), South Korea (an improved outlook for defence and electrical equipment), and China (favourable valuations).

However, over the medium to long term, India’s GDP growth outlook remains structurally strong. With a revival in corporate profitability and a tariff reset, we expect revival in FII interest going forward.

Q3. While large-cap equities have seen a relatively stronger recovery, mid- and small-cap segments have lagged. Do you believe valuations in the broader market still warrant caution, or are selective opportunities beginning to emerge as we look ahead?

Ans: Despite the time correction, Indian markets continue to trade above historical averages. However, with the expected improvement in corporate profits driven by a tariff reset, FTAs, and lower interest rates, we expect earnings to catch up with valuations going forward.

While the valuation premium to emerging markets remains elevated, it has corrected meaningfully over the past two years. This provides an opportunity for FIIs, whose current ownership in Indian equities stands below historical norms. Mid-caps offer the best risk-reward play, while small caps require a selective, bottom-up approach.

Q4. Multi-asset allocation funds have seen strong inflows over the past year. Do you believe this is largely driven by the recent performance of commodities within these portfolios, or does it reflect a deeper, structural shift in investor thinking around risk–return balance and diversification?

Ans: Recent inflows into multi-asset allocation funds have been driven by the recent performance of commodities and further amplified by the underperformance of Indian equities. However, we believe that, over the long term, equities provide better risk-adjusted and sustained returns. Commodity cycles remain volatile and relatively less predictable.

While multi-asset allocation funds do offer a balanced risk-return profile and diversification over the long term, sustained investor interest remains a function of the commodity cycle.

Q5. In equity mutual fund investing, periods of temporary underperformance are inevitable. How should investors evaluate such phases, and what role does patience play in achieving long-term outcomes?

Ans: The foundation of long-term wealth building lies in belief in the power of compounding, discipline in systematic investing, and the conviction that equities provide better long-term, risk- and inflation-adjusted returns. One’s conviction is often tested during periods of underperformance and sharp market declines.

History suggests that such periods present an opportune time to accumulate, given favourable valuations. Hence, patience remains the most important virtue in equity investing and long-term wealth building.

Q6. If SIPs are meant to counter behavioral biases in mutual fund investing, what single habit should investors adopt in the new year to improve long-term outcomes?

Ans: In the world of social media and influencers, investors are often swayed by advice that is either poorly timed or driven by malafide intent. Additionally, apps that provide real-time portfolio updates can amplify fear and trigger behavioral biases.

While it is difficult to completely avoid such influences, investors should remain focused on their long-term needs. Investors should align their return objectives with risk tolerance after discussion with their advisors.

Source: Internal Research

Mutual fund investments are subject to market risks, read all scheme-related documents carefully.

Imp.Note: We are registered NJ Wealth Partners and this interview published is sourced from NJ Wealth with due permissions. Reproduction of this interview/article/content in any form or medium by any means without prior written permissions of NJ India Invest Pvt. Ltd. is strictly prohibited.